Encash your Insurance at a higher price!

A pair of twill woven shorts featuring slanted front pockets, buttoned back pockets, a zip pocket, buttoned waist, and keychain loop.

Hihi mommies, some of us may have done some calculation and realise that 1) surrendering certain policies is better than continuing it until maturity...

some of us may have 2) policies which have incurred policy loan and interests or even policies which have lapsed due to non-payment of premiums...

some of us may have 3) better plans for the monies that are locked long-term in policies...

If you have decided not to continue with your insurance savings plan, now you have the option of CASHING OUT at a higher value than surrendering it!

If assessed to be suitable, you will be able to sell (“assign”) it to our partnering companies for a HIGHER AMOUNT than the value you would have received surrendering it back to the insurance company. It is estimated to be 5-10% higher.

Even if your policy is worth little to zero dollars in surrender value with the insurers, we may still be able to Unlock Cash and pay you Cash for the policy!

This may include policies which have lapsed or policies which have incurred policy loan and interests eating into its cash value.

At SGIM, we work with a few Insurance buyback partnering companies so that we can help you ensure that you MAXIMISE your SURRENDER VALUE of your policy(s).

Anyway, no worries, just fill up the form below first. ;)

We will get back to you within the next 2 working days whether your policy is suitable for to be sold for a value higher than the surrender value.

If you then decided to proceed, we will manage the process for you with immediate payment.

Process is as simple as 3 steps.

Step 1 - Submit Policy Details

Step 2 - Inform you on suitability and amount

Step 3 - Collect Cheque

FAQs

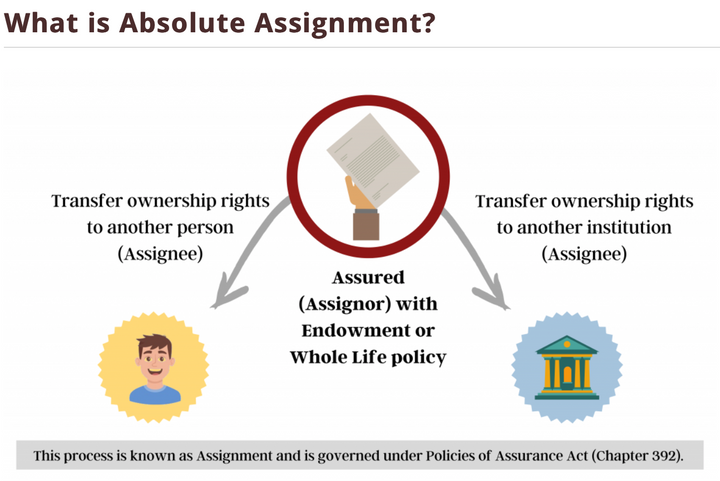

1) Is this legal?

Yes. This is a 100% legal transfer of all policy rights and benefits to the assignee, from the original policy owner.

An Absolute Assignment is the assigning of a policy to transfer the ownership rights from the Assured (Assignor) to another person or institution (Assignee). You can transfer the rights on your life insurance policy to another person or institution for various reasons. This process is known as Assignment and is governed under Policies of Assurance Act (Chapter 392). Endowment Policies and Whole Life Assurance Policies are assignable. Other types of insurance policies are generally non-assignable.

2) Why is it that we are able to get extra cash more than the surrender value?

Insurance policies such as Whole-life plans and Endowment plans are low-risk, stable assets and since the policy has been serviced for some time. It is using money to exchange for the time. It saves time as policy buyers do not need to buy from policy year 0.

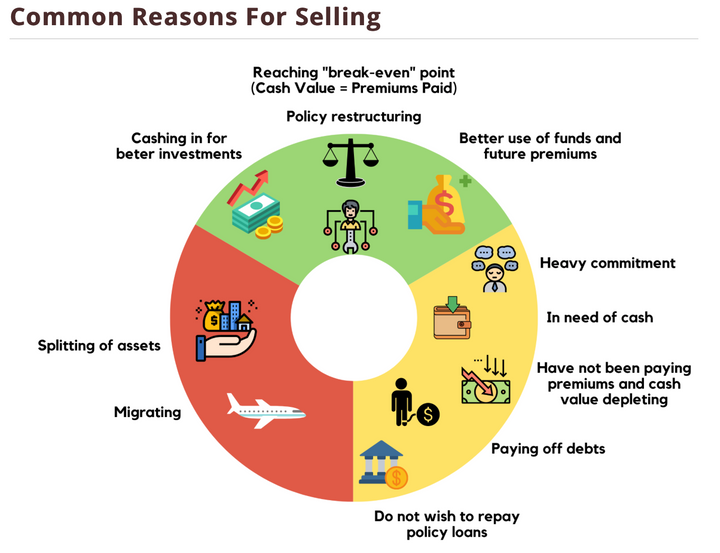

3) Why do people surrender policies?

People surrender policies for various reasons. One common reason is a discovery of a new policy that are more suited to their needs vs the older ones. Hence, they may like to switch to a new investment policy or other financial assets by liquidating the current asset. Most often, policy owners have found an alternative investment/ business opportunity that will bring them more returns, hence they want to cash out their existing policies.

Other reasons include 1) needing money for new business, 2) changes in financial circumstances, 3) need for emergency funds due to hospitalisation, 4) splitting of assets due to divorce, 5) unable to continue servicing the premiums etc.

4) Before submitting my policy details, can I roughly gauge on whether my policy will be suitable to en-cash?

Yes. As a general guide, this buyback scheme usually applies to only Savings/ Endowment plans and/or selective Whole-Life plans.

Investment-Linked Plans (Plans with names including "link") and/or plans like term plans, accidental plans, hospitalisation plans are not applicable.

If you have endowment plans or whole life plans, please send us the information here for us to confirm whether it qualifies. Be assured that if it qualifies, you will definitely get back more than what the insurers can surrender for you.

5) Does the life assured remain the same, since the policy owner changed?

Yes the life assured remains the same, so the death benefits will belong to the new policy owner. However, we do not advise the purchaser to buy with the expectation of this as this is very unknown. Purchasers buy traded endowment because of the better returns they can get as compared to restarting and buying a fresh policy from the start or to put their money in a fixed deposit in the banks.